Immediate context and why comparisons matter

Consumers in Mexico and beyond are turning to fast, app-based lending more often, and that shift brings real trade-offs. For many, didi prestamos represents a convenient way to access cash without branch visits. This article compares DiDi’s instant loan model against other online options and lays out the practical requirements you’ll meet before clicking “apply.” The tone here is factual but concerned: speed is valuable, yet speed without clear terms can be costly.

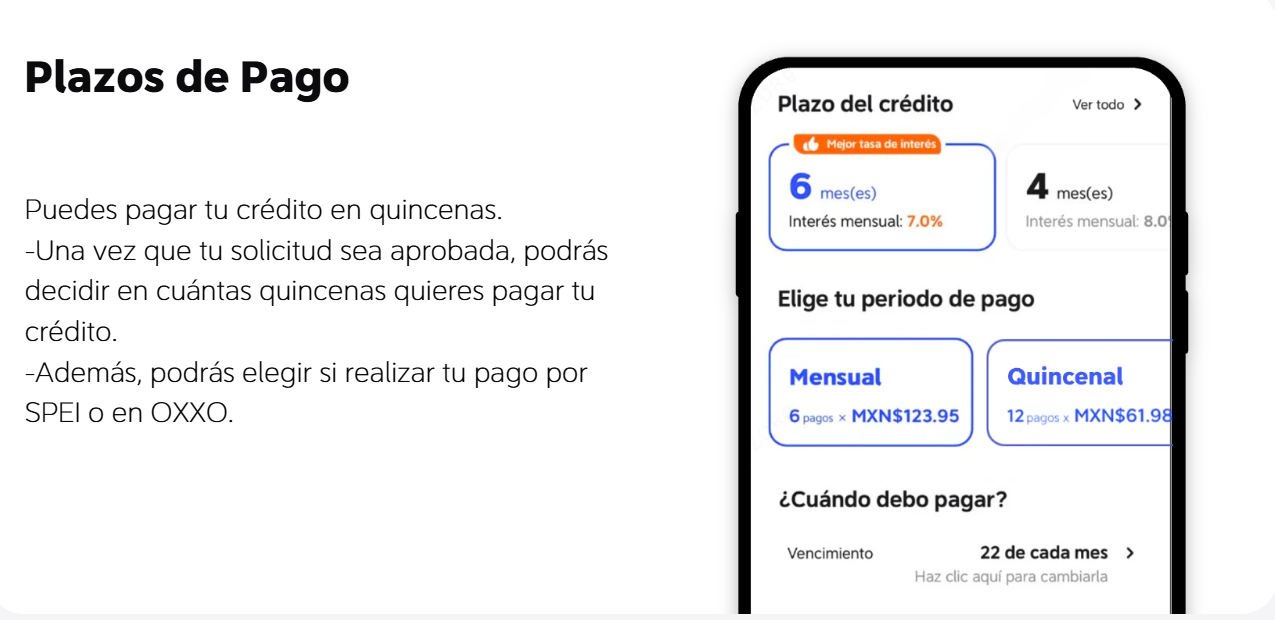

How DiDi loans work — the basics

DiDi’s offering centers on quick digital onboarding, automated underwriting, and rapid disbursement to mobile wallets or accounts. Typical steps are identity verification (KYC), a short credit check, then an approved amount with a stated APR and loan term. The process favors convenience: some applicants receive funds within hours. That convenience, however, often pairs with higher interest rates than traditional bank loans.

Eligibility and essential requirements

Requirements are straightforward but firm: government ID, proof of income or consistent transactions, and a linked bank account or mobile wallet. Lenders use credit score proxies and transaction history when formal credit files are thin. Expect requests for phone verification and consent for electronic records. These controls reduce fraud but also create friction for low-income users who rely solely on cash—this is a real equity issue, especially in dense urban centers like Mexico City where informal work is common.

Comparative insight: DiDi vs. other digital lenders

Compared with peer apps, DiDi scores high on speed and user interface clarity. Other lenders sometimes offer lower APRs but require longer approval times or stricter credit histories. Alternatives such as payroll-linked products or credit union digital loans can be cheaper but less accessible to gig workers. Consider these industry terms when comparing offers: APR, loan term, and underwriting criteria. Look beyond advertised rates to origination fees and late-payment penalties.

Common mistakes when choosing a digital loan

Borrowers often focus on the headline amount while ignoring total repayment. That leads to surprises at the end of the term. Another frequent error is skipping the fine print on automatic debit authorization—this matters when income varies. Read the repayment schedule; check for prepayment penalties. Also, avoid stacking short-term loans to cover ongoing expenses—a cycle that quickly snowballs. —It’s simple but easy to overlook when cash is tight.

Safety, regulation, and user protections

Digital lenders operate under consumer protection rules that vary by country. In Mexico, for instance, regulators stepped in after 2020 to tighten transparency following a rapid rise in app-based credit. That year remains a clear turning point for digital finance globally. Verified data from central banks and consumer agencies now inform better disclosure practices, but responsibility still rests with the borrower to verify terms and keep records of agreements.

Alternatives worth considering

If DiDi’s speed appeals but cost concerns you, compare these options: credit union microloans, employer payroll advances with fixed fees, or a secured line tied to a savings account. Peer-to-peer platforms may offer competitive APRs but involve slower funding. For gig workers seeking stability, a bank-backed overdraft or a small personal line from a local cooperative may be a safer long-term choice. And if you’re comparing offers, also scan for customer-service responsiveness—timely dispute resolution matters.

Advisory close: three metrics that should guide your choice

1) Total cost of credit: add APR, fees, and potential penalties to know the real price. 2) Repayment flexibility: check whether payment dates and amounts can adjust if income drops. 3) Transparency score: confirm clear disclosure of fees, automated debits, and data-sharing practices. Use these metrics to rank offers objectively.

DiDi Finanzas presents a viable instant option when you need speed and clear disclosure—evaluate it against the three metrics above, and choose what preserves your cash flow and peace of mind. –