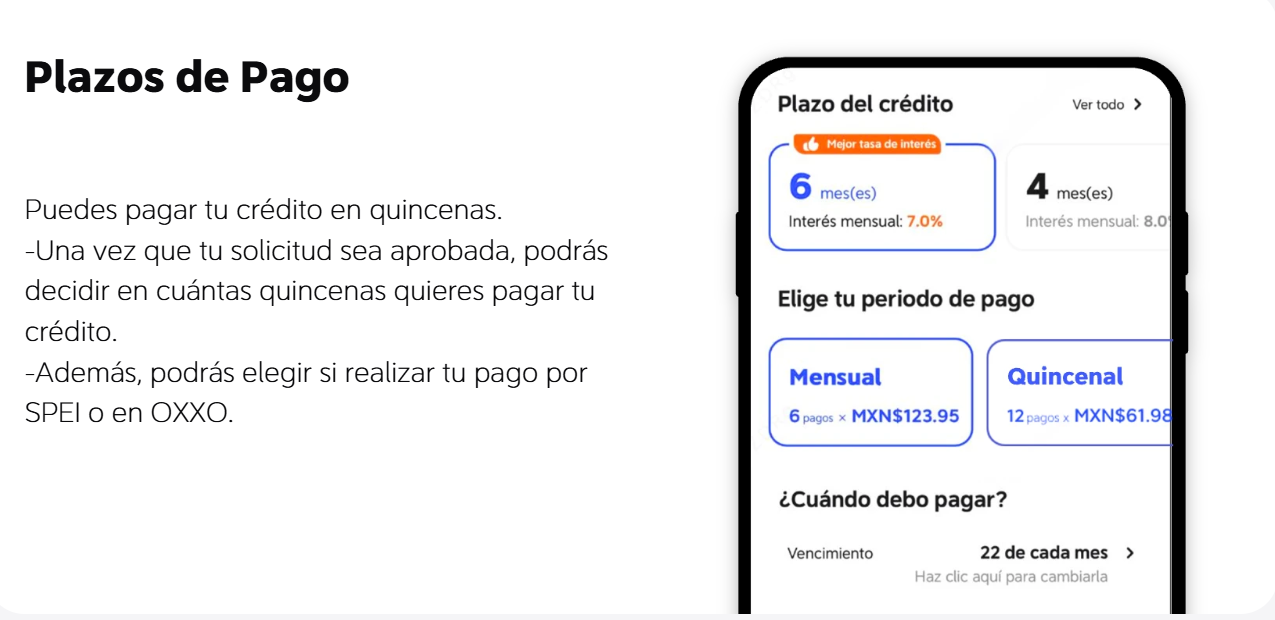

Comparative snapshot: what this comparison sets out to show

This piece compares tangible savings and rewards tied to platforms like DiDi Finanzas with standard bank and fintech options, using cautious, evidence-based language. Early indicators from user reports and platform disclosures suggest faster approval flows and integrated incentives on platforms linked to ride-hailing ecosystems; see didi prestamos for one example of loan offers integrated into a broader mobility service. The goal here is practical: identify where measurable cost or time savings appear, and where trade-offs remain.

Where hidden savings and rewards typically appear

Digital lenders aligned with large platforms often reveal savings that are not obvious on first glance. These include lower origination fees bundled into promotional offers, cashback or ride-credit rewards that offset recurring costs, and reduced administrative friction that cuts loan origination time. From an industry standpoint, APR and underwriting criteria matter most — a lower headline APR is useful only if fees, penalties, and repayment rigidity are also transparent. Evidence-based comparisons prioritize total cost of credit over single metrics.

User experience, onboarding, and risk trade-offs

Onboarding via a mobile app usually reduces friction: quick document upload, streamlined KYC, and automated credit decisions. That speed can improve access for drivers or gig workers who need immediate liquidity. But speed often correlates with lighter-touch underwriting and increased reliance on alternative data — which may lead to variable pricing tied to real-time behavior or occupation. Global surveys such as the World Bank’s financial inclusion work highlight how digital credit expanded rapidly after 2020; policymakers noted both benefits and new consumer risks. – A small aside: faster isn’t always fair if error-prone algorithms misprice risk.

How DiDi Finanzas compares to common alternatives

When placed against traditional banks, payroll- or merchant-linked credit, and payday-style offers, platform-tied products tend to win on convenience and rewards but may trail on dispute-resolution maturity and long-term interest savings. Alternatives to consider include local bank loans for lower long-term APR, credit unions with member-focused underwriting, and established fintech lenders with transparent amortization schedules. Common mistakes borrowers make: ignoring total repayment cost, failing to check return policies for rewards, and assuming app speed implies a cheaper loan.

Practical checklist before choosing a digital lender

Use this short checklist to evaluate offers: verify total repayment amount including fees; confirm how rewards reduce effective cost; check data policies and dispute channels. Industry terms to scan for include APR, loan origination fees, and credit score impact. Also verify whether rewards (ride credits, cashback) are redeemable where you need them — not all incentives offset the expenses you actually face.

Advisory: three critical metrics to evaluate digital lending options

1) Total cost of credit: Add APR, origination fees, and any mandatory insurance or processing charges to see true cost. Favor offers with clear amortization schedules rather than promotional headlines.

2) Speed with transparency: Fast loan origination is valuable, but require clear disclosure of underwriting criteria, penalty triggers, and reward redemption rules. Transaction time alone is not a reliability metric.

3) Data safety and dispute resolution: Confirm encryption standards, KYC protections, and an accessible complaint pathway. Platforms tied to large networks may collect broader telemetry — ensure consent and remedy options are explicit.

Conclusion

Evaluate each offer against these metrics and you’ll find which option delivers real savings versus temporary perks. For many users, the blend of rapid access and practical rewards that platform-linked services provide solves immediate needs while posing manageable trade-offs when monitored carefully — and that practical value is where DiDi Finanzas often fits naturally as part of a broader financial toolkit. –